The proposition that increased taxation on ultra-high-net-worth individuals can resolve national fiscal deficits relies on a fundamental misunderstanding of the relationship between paper wealth and liquid capital. While the optics of wealth concentration suggest a ready-made solution for budget shortfalls, the actual mechanics of capital flight, valuation volatility, and the "Denominator Problem" render such policies mathematically insufficient to address the scale of modern sovereign debt.

The Myth of Realizable Value

The core failure of the "tax the rich" narrative begins with the conflation of net worth and disposable income. Most high-level wealth is held in non-liquid assets—predominantly equity in private or public companies, real estate, and intellectual property. If you found value in this post, you should look at: this related article.

The Liquidity Gap

When a government mandates a wealth tax, it assumes that the underlying assets can be valued accurately and liquidated without market disruption. This ignores the Liquidity-to-Valuation Ratio. Forcing a founder to sell 2% of their company every year to pay a wealth tax creates a permanent "sell pressure" on the stock.

- Market Signal Distortion: Large, scheduled blocks of shares hitting the market signal a lack of confidence, even when the sale is tax-mandated.

- Capital Erosion: As share prices drop due to increased supply, the total tax base shrinks, creating a feedback loop where higher tax rates are required on a diminishing asset pool.

- The Valuation Trap: For private companies (unicorns), valuation is often a "mark-to-market" exercise based on the last funding round. Taxing a paper valuation that may disappear in the next down-round forces the liquidation of real assets to pay for imaginary gains.

The Three Pillars of Fiscal Ineffectiveness

If every billionaire’s net worth were seized tomorrow, the resulting windfall would cover the annual budget of a major G7 nation for less than eight months. This creates a structural mismatch between a one-time wealth grab and a recurring operational deficit. For another perspective on this story, see the recent update from Business Insider.

1. The Denominator Problem

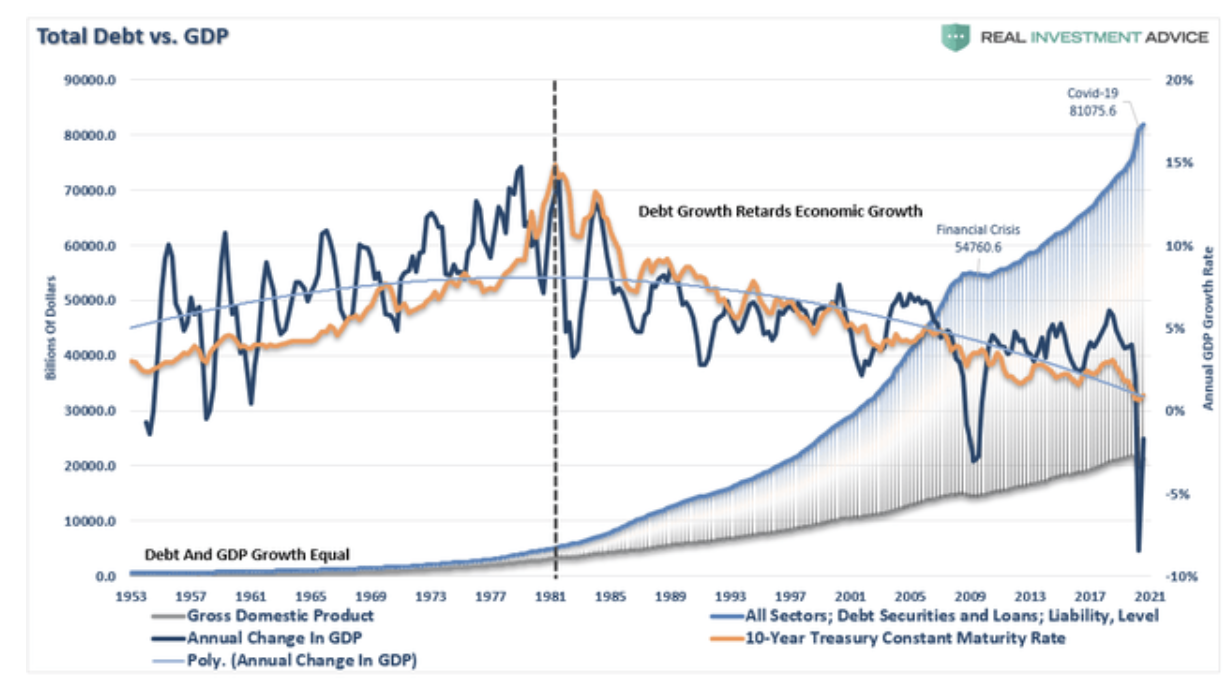

National debts are measured in trillions, while collectible annual revenue from wealth taxes is measured in billions. In the United States, the annual federal deficit frequently exceeds $1.5 trillion. Even the most aggressive wealth tax proposals estimate annual yields between $200 billion and $300 billion. The math dictates that even with 100% compliance, the deficit continues to grow. The tax does not solve the "mess"; it merely slows the rate of decay by a marginal percentage.

2. Capital Mobility and the Jurisdictional Arbitrage

Capital is a coward; it flees to where it is treated best. In a globalized economy, "taxing the rich" is effectively an invitation for Jurisdictional Arbitrage.

- Tax Residency Shifting: High-net-worth individuals (HNWIs) possess the resources to relocate their tax domicile to low-friction environments (e.g., Singapore, Dubai, or Switzerland).

- Asset Reclassification: Wealth is restructured into debt instruments, trusts, or foreign-held entities that sit outside the immediate reach of domestic tax authorities.

- Brain Drain: The loss isn't just the tax revenue; it’s the loss of the "Multiplier Effect" generated by the investment and consumption of these individuals within the local economy.

3. Administrative Friction and the Cost of Collection

The bureaucracy required to audit, value, and litigate the net worth of the top 0.1% is immense. Unlike income, which is captured via standard payroll (W-2) or basic reporting (1099), wealth is an amorphous target.

- Appraisal Wars: Determining the "fair market value" of a private art collection, a patent portfolio, or a bespoke hedge fund stake leads to years of litigation.

- The Net-Negative Yield: When the cost of enforcement, litigation, and the subsequent loss in capital gains taxes (due to depressed asset prices) is factored in, the "net yield" of a wealth tax often approaches zero or turns negative.

The Displacement of Private Investment

The most significant "hidden cost" of taxing concentrated wealth is the disruption of the Capital Allocation Cycle.

Private vs. Public Efficiency

Capital held by the wealthy is generally deployed into investment vehicles: venture capital, private equity, or capital expenditures for existing businesses. These investments drive innovation and employment. When that capital is extracted via taxation, it is moved from an active investment pool to a government consumption pool.

The government rarely "invests" tax revenue in a way that generates a compounded return higher than the private market. Instead, it uses the funds for service debt interest or social transfers. This effectively trades future economic growth for current-term deficit mitigation—a strategic error for any nation facing long-term demographic or competitive challenges.

The Revenue Volatility Trap

Revenue systems that rely heavily on a tiny sliver of the population are inherently unstable. This is the Concentration Risk of fiscal policy.

If the top 1% provides 40% of a nation’s tax revenue, the entire state budget becomes a derivative of the stock market. During a market crash, tax receipts plummet exactly when the government needs funds most for social safety nets. By shifting the tax burden further toward the wealthy, governments increase their exposure to market cycles, leading to more frequent and severe fiscal crises during downturns.

Structural Reform: The Only Viable Path

Solving a "mess" caused by structural overspending and stagnant productivity with a superficial tax on assets is like attempting to fix a leaking ship by painting the hull. The math does not support the outcome.

To move beyond the performative politics of wealth taxation, a nation must address the Velocity of Capital and Regulatory Friction.

- Broadening the Base: Sustainable revenue comes from a broad, low-rate tax system that encourages high participation and minimizes avoidance.

- Consumption-Based Models: Shifting from taxing "inputs" (work and investment) to "outputs" (consumption) via VAT or GST structures ensures revenue is captured at the point of exchange, making it harder to evade through residency shifts.

- Productivity Indexing: Government spending must be indexed to GDP growth and productivity metrics rather than inflationary expansion.

The fiscal "mess" is a function of a $34 trillion debt ceiling and an entitlement system built on 1950s demographics. No amount of wealth seizure can bridge that chasm. The strategic priority for any administration must be the aggressive expansion of the tax base through GDP growth, not the cannibalization of the existing capital stock.

The Strategic Play

Cease the pursuit of a wealth tax as a primary revenue generator. Instead, pivot to a "Capital Repatriation Framework" that offers lower corporate tax rates in exchange for mandated domestic infrastructure investment. This secures the capital within the borders and utilizes private-sector efficiency to solve public-sector problems without the administrative overhead of a wealth tax. Move the focus from "who has the money" to "where is the money being put to work."